Recently, a report posted on the Social Science Research Network found that 186 banks in the United States are at risk of failure or collapse due to rising interest rates and a high proportion of uninsured deposits. The report titled ‘Monetary Tightening and US Bank Fragility in 2023: Mark-to-Market Losses and Uninsured Depositor Runs?’ estimated the market value loss of individual banks’ assets during the Federal Reserve’s rate-increasing campaign. The study also examined the proportion of banks’ funding that comes from uninsured depositors with accounts worth over $250,000. This blog post aims to explore the implications of the report and why it matters to buyers and sellers.

The Risk of 186 Bank Failures in 2023

According to the report, if half of the uninsured depositors quickly withdrew their funds from these 186 banks, even insured depositors may face impairments as the banks would not have enough assets to make all depositors whole. This could potentially force the Federal Deposit Insurance Corporation (FDIC) to step in.

The failure of Silicon Valley Bank serves as an example of the risks posed by rising interest rates and uninsured deposits. The bank’s assets lost value due to the rate increases, and worried customers withdrew their uninsured deposits. As a result, the bank failed to meet its obligations to its depositors and was forced to close.

ALSO READ: List of Failed Banks in the United States

The report noted that “Even if only half of the uninsured depositors decide to withdraw, almost 190 banks are at potential risk of impairment to insured depositors, with potentially $300 billion of insured deposits at risk. If uninsured deposit withdrawals cause even small fire sales, substantially more banks are at risk.” The economists who conducted the study warned that these 186 banks are at risk of a similar fate without government intervention or recapitalization.

ALSO READ: Banking Crisis Explained: Causes of Bank Collapse & its Prevention

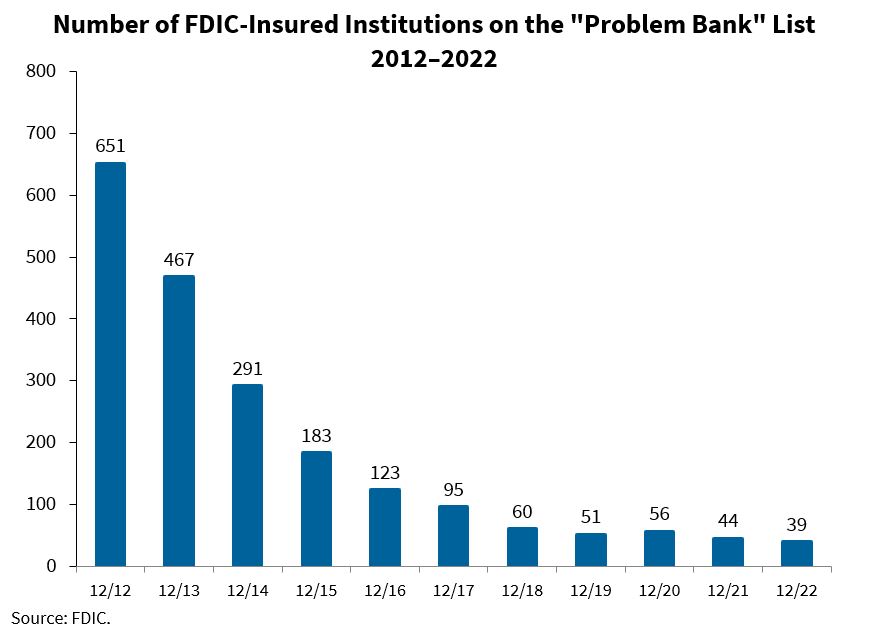

Number of FDIC-Insured Institutions on the “Problem Bank” List

The number of FDIC-insured institutions on the “Problem Bank” list has continued to decline over the years. In 2012, there were 651 problem banks, which decreased to 467 in 2013, 291 in 2014, and 183 in 2015. The trend continued with 123 problem banks in 2016, 95 in 2017, and 60 in 2018. By the end of 2019, there were 51 problem banks, and the number slightly increased to 56 in 2020. However, in 2021, the number dropped to 44. Looking ahead to 2022, the number of problem banks continued to decline, reaching 39 by the end of the year. This decline in problem banks is a positive trend for the banking industry and the economy as a whole.

| Month/Year | Number of Problem Banks |

| 12/12 | 651 |

| 12/13 | 467 |

| 12/14 | 291 |

| 12/15 | 183 |

| 12/16 | 123 |

| 12/17 | 95 |

| 12/18 | 60 |

| 12/19 | 51 |

| 12/20 | 56 |

| 12/21 | 44 |

| 12/22 | 39 |

As of 2023, the latest available data on the number of FDIC-insured institutions on the “Problem Bank” list is for the year-end 2022. According to the FDIC’s reports, the number of problem banks continued to decline, reaching 39 by the end of 2022. This is a positive trend for the banking industry, indicating its stability and resilience amidst various economic challenges. The banking industry will continue to face risks and uncertainties, but the decreasing trend in problem banks demonstrates the effectiveness of the regulatory framework in ensuring the safety and soundness of the financial system.

Silicon Valley Bank Failure in 2023

Silicon Valley Bank, once a prominent player in the banking industry, collapsed after struggling to cope with rising yields that eroded the value of its assets. The bank was shut down by Californian regulators, and the FDIC was appointed as the receiver. This marks the largest bank failure since the financial crisis of 2008 when Washington Mutual went bust.

Silicon Valley Bank attempted to recover from its losses by selling a portfolio of treasuries and mortgage-backed securities to Goldman Sachs at a loss of $1.8 billion. However, it failed to raise $2.25 billion in common equity and preferred convertible stock to plug the hole. The bank’s clients became increasingly worried and withdrew their deposits, causing $42 billion in outflows in just one day.

In an attempt to salvage its businesses, Silicon Valley Bank announced earlier this week that it was exploring strategic alternatives for its holding company, SVB Capital, and SVB Securities. The company said that SVB Securities and SVB Capital’s funds and general partner entities were not included in the Chapter 11 filing. The company added that it planned to proceed with the process to evaluate alternatives for its businesses, as well as its other assets and investments.

Potential Impact of Such Bank Failures

The findings of the report highlight the importance of careful risk management and diversification of funding sources for banks to ensure their stability in the face of market fluctuations. Buyers and sellers of banking assets should carefully evaluate the risks associated with uninsured deposits and the potential impact of rising interest rates on bank assets.

The failure of Silicon Valley Bank serves as a cautionary tale for the banking industry, and it is essential to take proactive steps to mitigate the risks posed by these factors. The government may also need to step in to prevent a similar fate for the 186 banks identified in the report.

The potential impact of nearly 200 banks being at risk for the same fate as Silicon Valley Bank could be significant for the banking sector and the broader economy. If a large number of these banks were to fail, it could lead to a domino effect, causing other banks to fail as well. This could lead to a credit crunch, making it difficult for businesses and consumers to access credit and slowing economic growth.

In addition, a bank run on one of these vulnerable institutions could cause a ripple effect, causing depositors to withdraw funds from other banks as well. This could lead to a broader panic and a loss of confidence in the banking system as a whole, potentially leading to a recession or even a financial crisis. The federal government’s promise to back all depositors in these banks is a step in the right direction to help prevent a wider panic.

However, this may not be enough to prevent a bank run if customers believe that the bank is insolvent. It is important for regulators and policymakers to monitor the situation closely and take action to prevent further bank failures. This could include recapitalizing vulnerable banks or providing government guarantees to support their operations. Overall, the situation highlights the importance of a stable banking system and the need for effective risk management practices in the financial sector.

ALSO READ: Bank Failures in 2023: Why it Can’t Crash Real Estate?

Sources:

- https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4387676

- https://www.fdic.gov/analysis/quarterly-banking-profile/qbp/2022dec/chartdif2.xlsx

- https://www.businesstoday.in/industry/banks/story/186-us-banks-at-risk-of-failure-similar-to-silicon-valley-bank-says-research-heres-why-373895-2023-03-18