Last week Statistics Canada confirmed that our GDP increased by 0.1% in February on a month-over-month basis (MoM).

Last week Statistics Canada confirmed that our GDP increased by 0.1% in February on a month-over-month basis (MoM).

The result was a little better than the flat reading expected by the consensus, but it was still well below the 0.6% MoM increase we saw in January. Stats Can now also expects that our GDP will have decreased by 0.1% MoM in March.

Our slowing economic momentum doesn’t come as a surprise.

The Bank of Canada raised its policy rate from 0.25% in March 2022 to 4.5% by January 2023, and BoC Governor Tiff Macklem has warned that those hikes will cause economic pain for Canadians as they work their way through our economy. (He is always quick to add that the pain of higher rates is preferable to the pain that will accrue if inflation is left unchecked.)

In fact, the surprise has been that it has taken this long for our momentum to shows signs of slowing.

Our economic data has been defying consensus economic forecasts as our job market continued to surge, consumers continued to spend, and our economy continued to grow. But with inflation now falling and our GDP approaching stall speed, will the BoC adopt a more dovish stance, and will the rate cut that our bond market is still expecting at the end of 2023 ultimately materialize?

Over the last several decades, there has typically been a gap of about six months between the BoC’s last policy-rate hike and its first cut.

If past is prologue, a BoC rate cut in the second half of this year will be in the cards. If that signals the start of an easing cycle, how many rate cuts might follow? More importantly for readers of this blog, does slowing economic momentum mean that Canadian mortgage borrowers should be reconsidering variable-rate options?

I have been a proponent of variable rates for most of my 13-year career as a mortgage broker, but I am still reluctant to adopt that view against our current backdrop.

For starters, while it is true that inflation is finally on the back foot, BoC Governor Macklem has repeatedly insisted that it must drop all the way to the Bank’s 2% target before rate cuts will be on the table.

As I wrote in last week’s post, the Bank would be sacrificing its already wounded credibility if it backtracks from that pledge. Also, while base effects will likely cause inflation to hit 3% by this summer, reducing it further from 3% to 2% will be much tougher – especially when wages are still rising by about 5% and large union contracts are being contentiously renegotiated.

Investors have become accustomed to central bankers having their backs when economic momentum slows. Since the Great Recession in 2008, bad economic news has been viewed as good news for financial markets because it portended the continuation and/or expansion of loose monetary policies that would juice investment returns.

But inflation was low and benign throughout most of that period, and that is no longer the case. Above-target inflation has significantly altered our central banker’s cost/benefit analysis.

At the same time, US influences are also helping to keep our fixed mortgage rates low, thereby reducing the impact of the BoC’s policy rate raises and likely delaying the onset of rate cuts.

Our Government of Canada (GoC) bond yields trade in lockstep with their US equivalents. When the US banking crisis hit last month, GoC bond yields plummeted, along with the fixed mortgage rates that are priced on them. While that impact on financial markets has largely abated, another US crisis may be looming.

The US Congress must once again vote to raise the federal government’s debt ceiling, and the Republican Party, which controls the House of Representatives, is refusing to do so. As various stop-gap funding measures are exhausted and the US federal government draws closer to default, investment capital will once again flow into safe-haven assets such as US Treasuries and GoC bonds. (And yes, the irony of a US debt default causing US Treasury yields to fall instead of rise is not lost on me. This an example of the exorbitant privilege that is unique to the Greenback as the world’s reserve currency.)

While few expect a US debt default to happen, no one seems entirely sure that it won’t. The level of brinkmanship today in the US Congress isn’t inspiring much confidence – it reminds me of Robin Williams’ old quip that Canada is a nice apartment living over a meth lab.

For now, variable rates still seem like an aggressive bet to me. Instead, I think three-year fixed rates strike the right balance because they are among the lowest rates currently available today. They provide protection from elevated near-term volatility and they are less likely to leave a borrower locked in for an extended period after rates have receded (as I think fixed-rate terms of five years or longer may end up doing). The Bottom Line: GoC bond yields were range-bound last week but that may change when the US Federal Reserve makes its next policy-rate announcement this Wednesday. (The market expects a quarter point hike and the announcement of a subsequent pause, but I think the Fed may surprise by sounding more hawkish than expected.)

The Bottom Line: GoC bond yields were range-bound last week but that may change when the US Federal Reserve makes its next policy-rate announcement this Wednesday. (The market expects a quarter point hike and the announcement of a subsequent pause, but I think the Fed may surprise by sounding more hawkish than expected.)

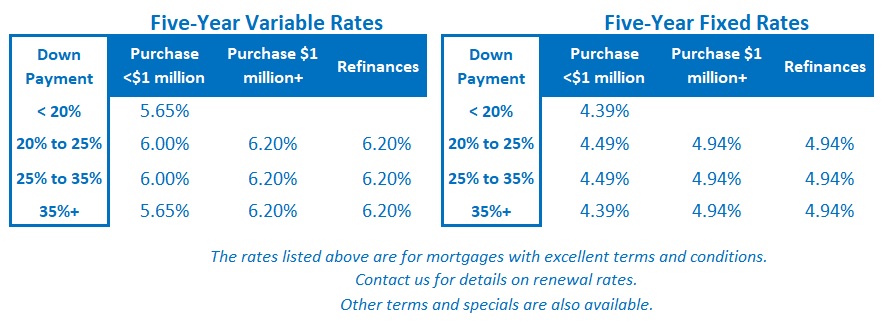

Fixed mortgage rates held steady last week, as did variable-rate discounts.

I continue to believe that rate cuts won’t materialize until at least 2024, and for the reasons outlined above, I view three-year fixed rates as the safest middle-of-the-road option.

For any who might be interested, here is a link to my wide-ranging interview last week with Strictly Money anchor and host Saijal Patel.

In it, Saijal asks me about falling mortgage rates, hot GTA house prices, the BoC’s next rate move, the stress test, housing affordability problems and potential solutions, and advice for frustrated young people who are trying to get into the housing market.