As we move into Winter and the start of a new year, expectations are not particularly high for the housing market. Home sales are expected to decline further following a sizeable decline in 2022. The outlook for pricing is weaker than in prior years in the most optimistic projections, with many forecasters and even many consumers anticipating declines in home prices.

Despite broad concerns, some economic data remain relatively sanguine. In a sharp contrast to sluggish home construction, the labor market continues to boast a low unemployment rate, which is driving nominal if not real wage gains for workers. Meanwhile, homeowners still enjoy record high levels of home equity.

The economy has yet to feel the full effects of the Fed’s tightening cycle due to the long lags with which monetary policy operates. However, the retreat in longer term interest rates, including mortgage rates, from early November peaks suggest that investors are calibrating for the end of the tightening cycle that drove rates higher. Mortgage rates are already down nearly 100 basis points from November. Still, real financial hurdles persist for many potential home shoppers. The typical 30-year fixed mortgage rate remains more than 250 basis points higher than one year ago and alongside continued, albeit moderating, home price gains, it has increased the cost of a monthly mortgage payment relative to one year ago. High housing costs and ongoing inflation have focused buyers on affordable markets, as noted in previous Emerging Housing Market Index releases.

Against a backdrop of an adjusting economy, the Wall Street Journal/Realtor.com Emerging Housing Markets Index highlights housing markets that offer shoppers a lower cost of living, including for homes, relatively steady real estate indicators amid a broader market in flux, and thriving local economies that are attractive, but not too crowded. The index identifies markets that those considering a home purchase should add to their shortlist–whether the goal is to live in it or rent it as a home to others.

We reviewed data for the largest 300 metropolitan areas in the United States. The Winter 2023 ranking surfaced the following top areas:

With home prices still high, inflation easing but still climbing faster than is typical, Winter 2023’s emerging markets offer residents a refuge from high costs. Home list prices in all but four of the top 20 markets are lower than the median-priced U.S. home for sale, which was $400,000 in December. Furthermore, the overall cost of living is nearly 8% lower than the national average. Some locales such as Kingsport-Bristol-Bristol, Tenn.-Va. offer just over 14% savings compared to the national cost of living. While the effective property tax rates in these markets are in line with the U.S. average at 1%, the estimated dollars paid are roughly half as low as we saw in Winter 2022, when lower real estate tax rates could not offset the impact of pricier housing markets.

With the housing market nationwide rebalancing in the face of still high mortgage rates and home prices, home sales have declined sharply and inventories have grown, prompting a slowdown in price growth and even price declines in some markets. The emerging markets are not immune to these adjustments, but market indicators have been somewhat steadier.

The average increase in homes for sale across the top 20 markets is 21% compared to more than 30% nationwide compared to the prior year. Among the top 20, seven saw the number of homes on the market climb faster than the national average, including the top three markets: Lafayette-West Lafayette, Ind., Fort Wayne, IN, and Elkhart-Goshen, IN

Although 11 of the top 20 emerging markets saw an increase in time on market, homes sold on average 10 days faster than the average across the 300 markets ranked for the index (34 vs. 44 days). Additionally, all 20 markets outperformed this national average.

The median price of the typical home for sale is still higher on a year-over-year basis nationwide and this is even truer among the top markets. All 20 markets saw double-digit price growth that averaged 8.6 percentage points faster than the average for the 300 markets (22.5% vs. 13.9%).

This quarter’s emerging markets are smaller than in the previous quarters with an average population roughly half that of the 300-market average. Only two of the top 20 markets have more than a million residents: Columbus, Ohio and Milwaukee-Waukesha-West Allis, Wis. Even at a time when the nationwide jobs market continues to register a long-time low in the unemployment rate, markets with healthy economies rank highly. All but one of the top 20 markets had an unemployment rate below the 300-market average (3.6%) and on average unemployment in the top 20 emerging markets was just 3.0%. Even though these areas have few out-of-work job seekers, commutes are relatively easy, clocking in at just less than 22 minutes compared to nearly 24 minutes on average across all markets in the index. Typical wages lagged behind the U.S. with an average weekly wage of $1,070 among the top markets compared to $1,100 among the broader market average. But this roughly 3% gap in wages is made up for in the cost of living differential. As a result of healthy wages, small businesses thrive in the top 20 areas with more than 57 SBA 7(a) loans per 1 million people compared to just 51 among the markets in the broader index.

Following several quarters in which strong demand from outside the local market was the norm for top emerging markets, this winter’s top markets, on average, are a near match to the average across all markets (70.2% vs. 70.8% overall). While some markets like Savannah, Ga. and Fall 2022 number one market Johnson City, Tenn. attract an outsized share of shoppers from elsewhere, others including Columbus, Ohio and Milwaukee-Waukesha-West Allis, Wis. rely more on local housing demand. Reflecting the broad trend of flexibility in location among home shoppers, both the top emerging markets and broader index markets have seen the share of out-of-market shoppers grow more than 7 percentage points compared to one year ago.

Bucking a previous hallmark of the emerging markets, Winter 2023 markets have residents who are, on average, no more mobile than residents in the top 300 markets with the share of those staying put and moving, 86.5% and 13.5% respectively, lining up. Two exceptions to this trend are Columbia, Mo. and this quarter’s number one market, Lafayette-West Lafayette, IN. In each of these markets, more than 1 in 5 residents live in a different house than one year ago.

Situated along the Wabash River in the western side of Indiana, Lafayette-West Lafayette, IN is roughly 60 miles northwest of the Indiana state capitol along I-85 and roughly twice as far southeast of Chicago. Just over 200,000 residents call this area home. Mirroring the trend seen in Realtor.com’s Top Housing Markets of 2023 report, the Lafayette-West Lafayette area is a manufacturing hub whose workforce also contains a higher share of government workers. Nearly 1 in 5 employees in Lafayette-West Lafayette works in manufacturing (18.7%), a higher share than statewide (16.8%) and nationwide (8.4%). Major local employers include Purdue University, renowned for its engineering program, Suburu of Indiana Automotive, Caterpillar Inc. and Wabash National Corp.

The typical home listed for sale in Lafayette and West Lafayette in December was priced just under $300,000, a nearly 25% discount over the December national median home list price of $400,000. Although the housing market has slowed compared to one year ago as the number of listings climb, the buyers and sellers in the Lafayette and West Lafayette market see shorter time on market than is common in many other areas.

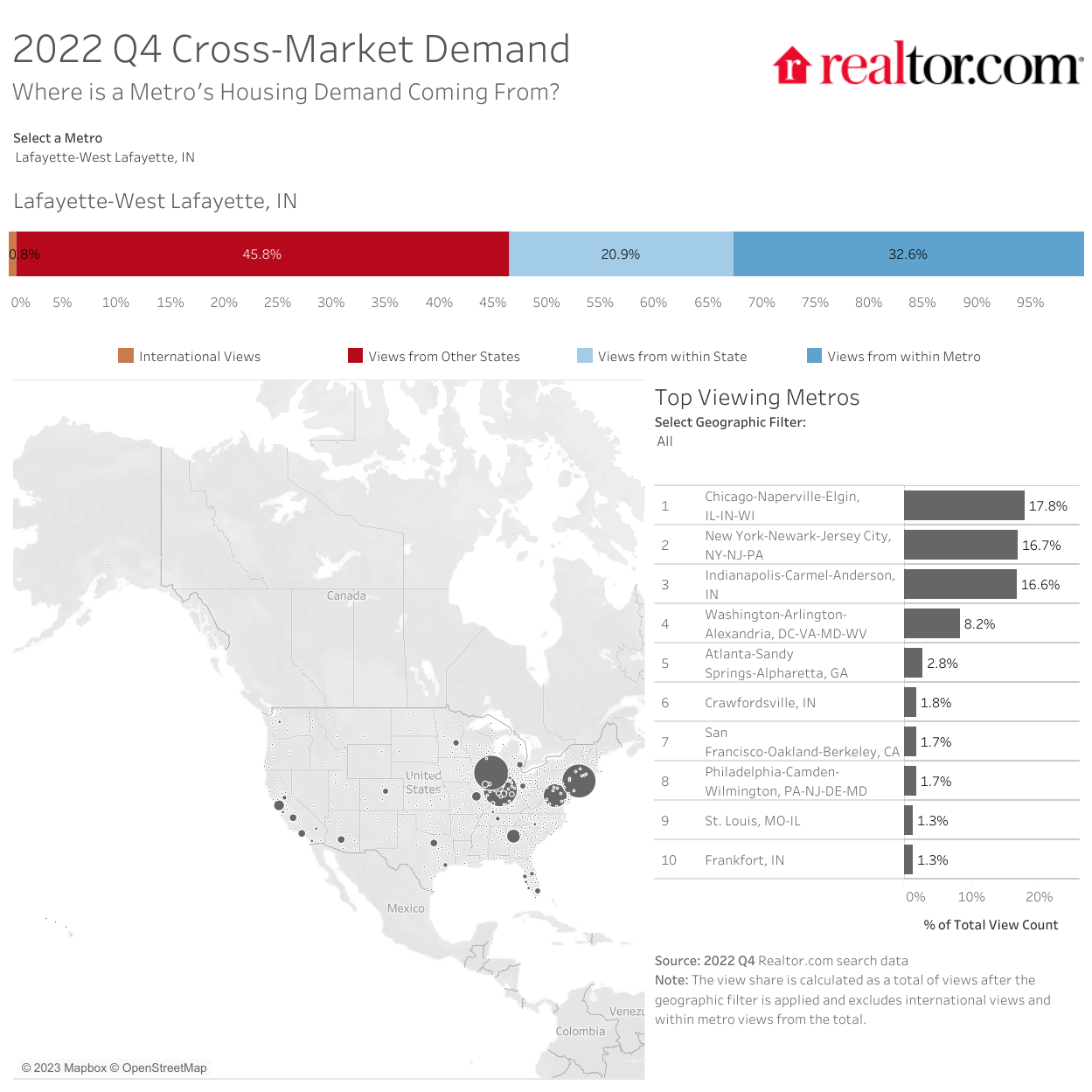

While the population in Lafayette-West Lafayette is more mobile, its share of out-of-state home shoppers is modestly lower than the 300 market average. Still, it’s not insignificant. Roughly 2 of every 3 home shoppers (67.4%) looking for homes are browsing from a different location. Out-of-market shoppers tend to come from higher cost metros with nearby Chicago and Indianapolis each contributing a large share. Together with home shoppers from the New York City metropolitan area, they make up over half of the out of market shopping interest in Lafayette-West Lafayette.

In addition to Purdue University sporting events, Lafayette and West Lafayette are home to gardens, museums, a zoo, and Samara House, a Frank Lloyd Wright designed home. Bikers and cyclists will enjoy the Wabash Heritage Trail which follows along the namesake river.

There are many familiar places on the list of the top 20 emerging markets: 8 members of the Fall 2022 list, most notably number 1, Lafayette-West Lafayette, Ind. This quarter’s number one market rose from number 6 on the fall ranking. Among the markets that have remained on our list are the ever-popular southern locales Burlington, N.C., last quarter’s number one market, Johnson City, Tenn., as well as the midwestern hotspot of Columbus, Ohio, and various small- to mid-sized midwestern cities that offer affordable housing and low costs of living.

Of the 12 markets that did not remain on the list from the Fall into the Winter, 5 tumbled a bit but remained in the top 50. The two biggest movers, Cape Coral-Fort Myers, Fla. and Naples-Immokalee-Marco Island, Fla., which fell 164 spots and 171 spots, respectively dropped into the bottom half of areas studied, ranking 177th and 187th this quarter. The markets that departed the top 20 in our index are mostly southern markets, including 5 Florida markets, as well as Columbia, S.C., Fayetteville-Springdale-Rogers, Ark.-Mo., Nashville-Davidson–Murfreesboro–Franklin, Tenn., and Raleigh, N.C.. The other 3 markets that fell out of favor were the Western markets of Visalia-Porterville, Calif., Colorado Springs, Colo., and Yuma, Ariz.. As economic conditions have changed since earlier in the year, with mortgage rates rising sharply, these relatively expensive markets have fallen out of favor and low-priced Midwestern markets have taken their place.

Taking the places of the 12 descended markets are the Southern locales of Savannah, Ga., Kingsport-Bristol-Bristol, Tenn.-Va. and Knoxville, Tenn., seven relatively affordable Midwestern towns, and the Northeast hotspots of Manchester-Nashua, N.H. and Portland-South Portland, Maine. Half of the markets ascended from within the top 50, but Springfield, Ill., Milwaukee-Waukesha-West Allis, Wis., La Crosse-Onalaska, Wis.-Minn., South Bend-Mishawaka, Ind.-Mich, Sioux City, Iowa-Neb.-S.D. and Rapid City, S.D. made larger jumps from the Fall rankings to land among the top of our Winter list. Much like the markets that stayed in the top 20, those that joined it tend to be more affordable. An interesting development is the swapping of higher-price Nashville-Davidson–Murfreesboro–Franklin, Tenn. for the more affordable Tennessee towns of Kingsport-Bristol-Bristol, Tenn.-Va. and Knoxville, Tenn..

The ranking evaluates the 300 most populous core-based statistical areas, as measured by the U.S. Census Bureau, and defined by March 2020 delineation standards for eight indicators across two broad categories: real estate market (50%) and economic health and quality of life (50%). Each market is ranked on a scale of 0 to 100 according to the category indicators, and the overall index is based on the weighted sum of these rankings. The real estate market category indicators are: real estate demand (16.6%), based on average pageviews per property; real estate supply (16.6%), based on median days on market for real estate listings, median listing price trend (16.6%). The economic and quality of life category indicators are: unemployment (6.25%); wages (6.251%); regional price parities (6.25%); the share of foreign born (6.25%); small businesses (6.25%); amenities (6.25%), measured as per capita “everyday splurge” stores in an area; commute (6.25%); and estimated effective real estate taxes (6.25%).

Join our mailing list to receive the latest data and research.

Winter 2023 Wall Street Journal/Realtor.com Emerging Housing … – Realtor.com News

(Visited 2 times, 1 visits today)