Realtor.com®’s October housing data release reveals that the inventory of homes that are actively listed for sale continued to grow and caught up to 2020 levels. However, this growth in active inventory was primarily due to the typical home spending more time on the market than last year, as seller sentiment remained muted and fewer homes were listed compared to the previous year. Listing price growth remained within the double-digits but continued to moderate.

Homes Actively For Sale Continue to Increase but Not Due to New Listings

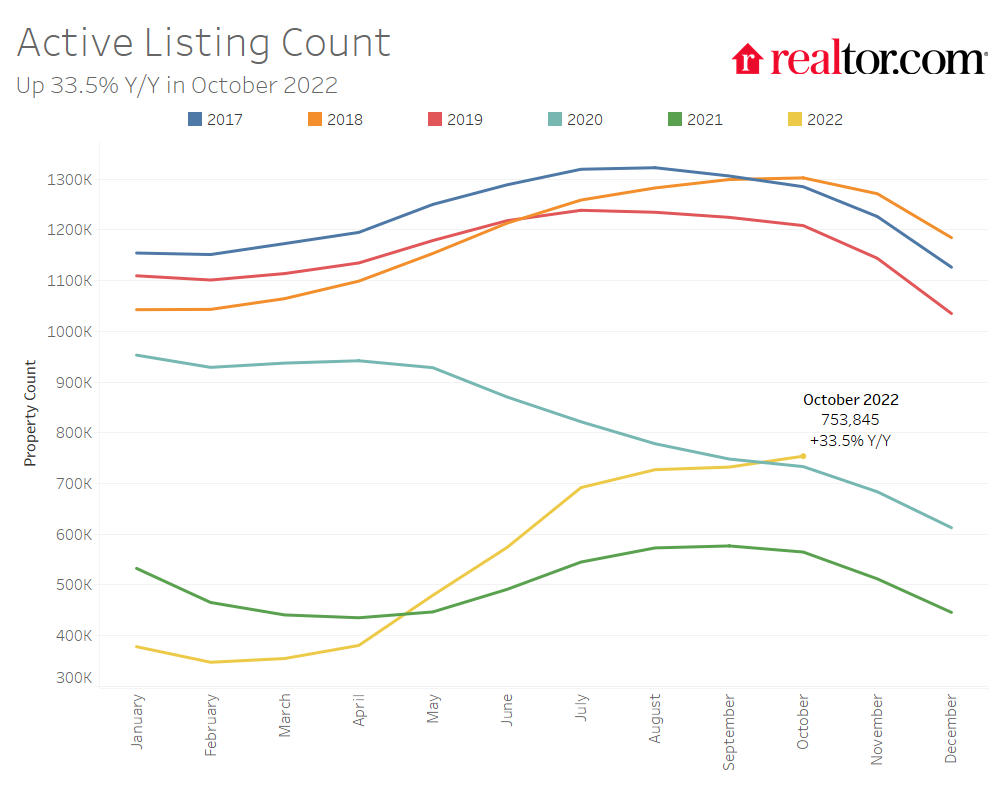

Nationally, the inventory of homes actively for sale on a typical day in October increased by 33.5% over the past year. This amounted to 189,000 more homes actively for sale on a typical day in October compared to the previous year. The growth rate of inventory increased compared to last month’s growth rate of 26.9% and has just surpassed 2020 levels.

Despite this improvement in the number of homes actively for sale, active listings still lag their pre-pandemic levels. The number of homes actively for sale in October was 40.4% lower than the pre-pandemic 2017-2019 average.

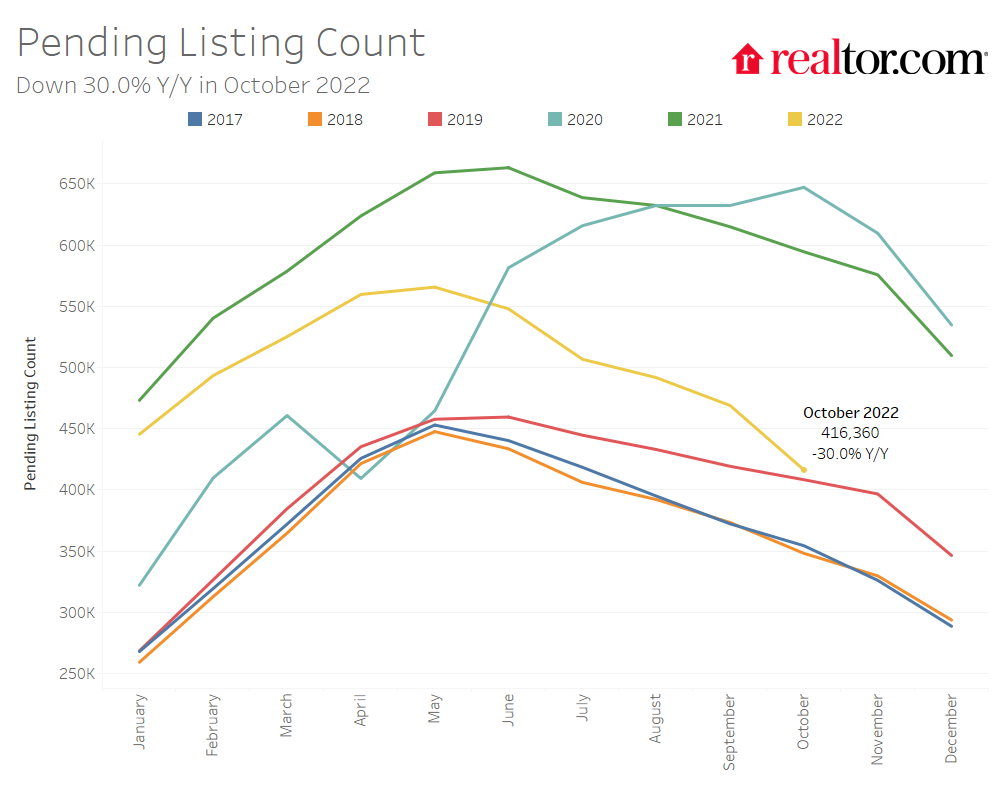

The total number of unsold homes nationwide—a metric that includes both active listings and listings in various stages of the selling process that are not yet sold—increased by only 0.5% year-over-year. Growth decelerated from last month’s 0.7% positive growth rate as the count of pending listings and newly listed homes fell further on a year-over-year basis.

The total inventory of homes for sale includes homes in pending status, which are those listings in various stages of the selling process that are not yet sold. The inventory of pending listings on a typical day has declined by 30.0% compared to last October. This is a further deceleration from the 23.7% annual decline we reported for September and the count of pending listings is approaching pre-pandemic 2019 levels. The decline in buyer demand has been spurred by rising interest rates and continuously growing home list prices that have increased the cost of financing 80% of the typical home by nearly $1,000 each month or 77.1% compared to a year ago, far outpacing recent rent growth (7.8%) and inflation (8.2%).

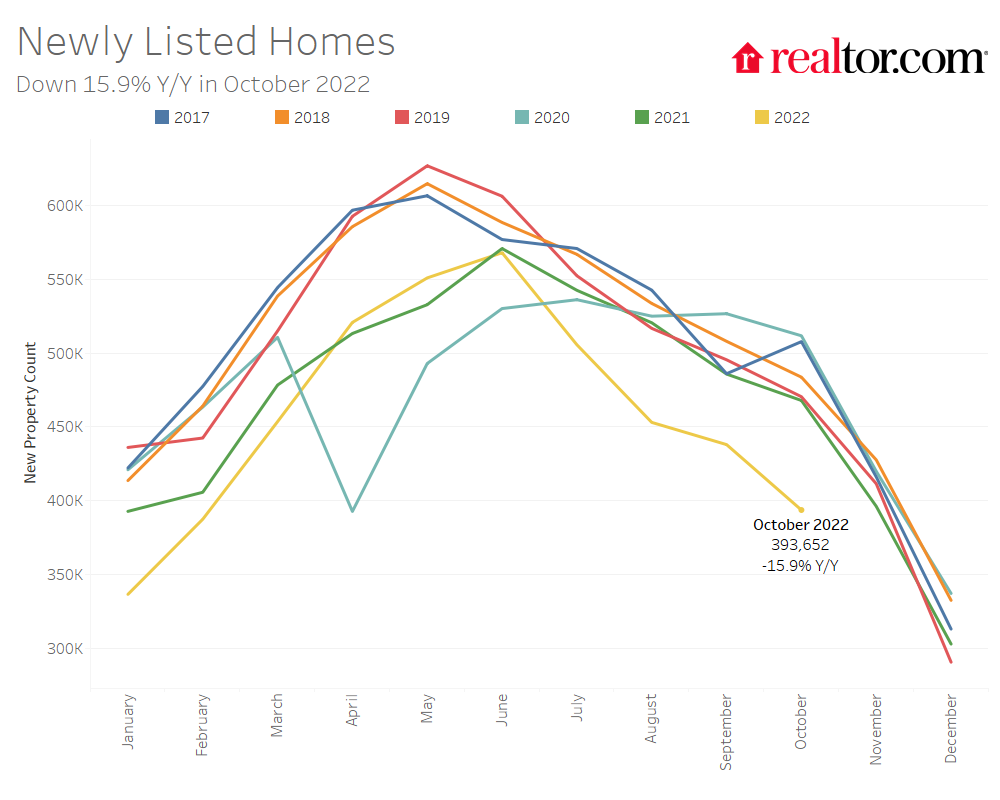

In October, newly listed homes declined by 15.9% compared to the same time last year, a greater rate of decline compared to last month’s 9.8% year-over-year decrease. In September, seller sentiment improved slightly but remained well below last year’s levels. Fannie Mae’s Home Purchase Sentiment Index (HPSI) revealed that the net share of respondents saying now is a good time to sell increased by 2 percentage points compared to the previous month but decreased by 29 percentage points compared to last year. The HPSI survey also revealed that the net share of Americans who believe home prices will go up over the next 12 months decreased by 3 percentage points in September compared to the previous month and by 16 percentage points compared to last year.

The inventory of homes actively for sale in the 50 largest U.S. metros overall increased by 46.4% over last year in October, outpacing the national growth rate. However, the inventory of homes in large Northeastern metros declined by 1.2% on average compared to last year, while other regions saw growth in the number of homes for sale. In the West, active listings grew most (by +72.1% year-over-year), closely followed by the South (+69.9%), with the Midwest growing more slowly (+12.4%). No regions saw new listing activity above the previous year. The South saw newly listed homes decline least, by 9.8% compared to the previous year, while they declined by 20.6% in the West, 17.4% in the Northeast, and 15.0% in the Midwest.

Inventory increased in 42 out of 50 of the largest metros compared to last year. Metros which saw the most inventory growth include Phoenix (+173.9%), Raleigh (+167.4%), and Nashville (+145.0%). Inventory is still declining on a year-over-year basis in 8 markets including Hartford (-25.7%), Virginia Beach (-11.0%), Milwaukee (-9.6%), and Chicago (-9.6%).

Only 4 of the 50 largest metros saw the number of newly listed homes increase compared to last year. The markets which reported year-over-year growth in newly listed homes were all Southern: Nashville (+10.5%), New Orleans (+6.2%), Dallas (+5.6%), and San Antonio (+1.4%). New Orleans was recovering from Hurricane Ida at this time in 2021. Markets which reported large declines in newly listed homes compared to last year included Western metros like San Jose (-36.1%), Sacramento (-29.7%), and San Francisco (-29.4%).

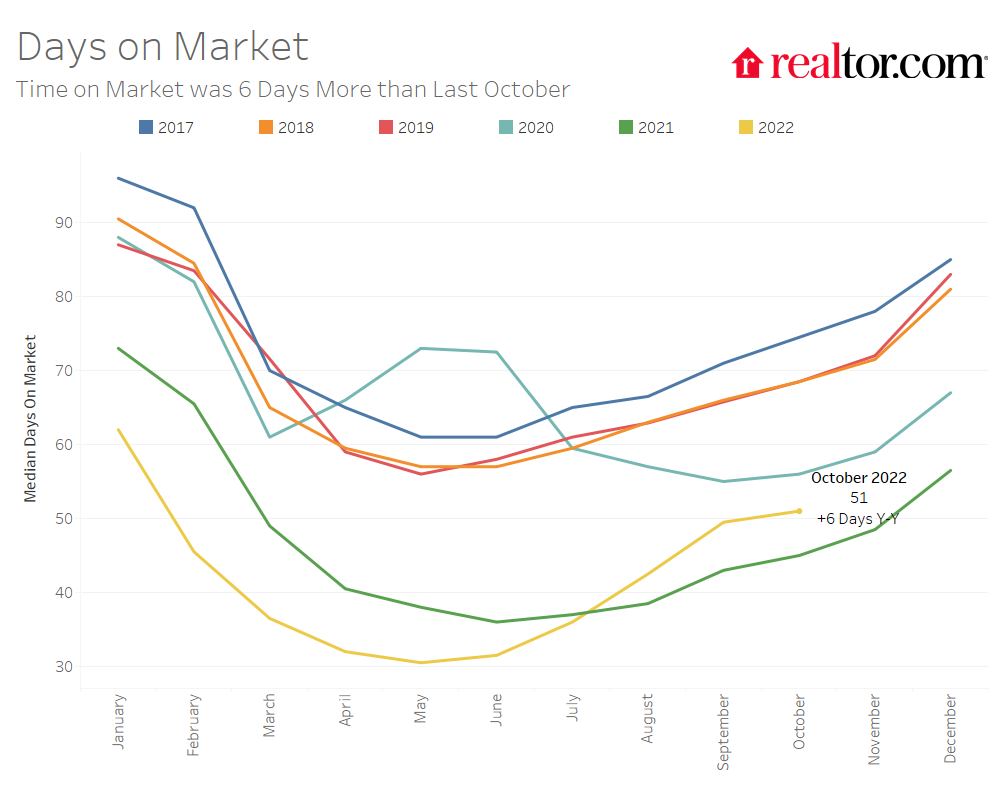

Home Listings Are Spending More Time on the Market

The typical home spent 51 days on the market this October which is 6 days more than last year. Slower inventory turnover is primarily fueling the growth in actively listed homes but homes still spent 20 fewer days on the market this October than typical 2017 to 2019 timing.

In the 50 largest U.S. metros, the typical home spent 45 days on the market, 6 days more than last October, with the slowdown matching the national rate. The time a typical home spends on the market increased across regions, with larger metros in the West seeing the greatest increase (+11 days), followed by the South (+6 days), Northeast (+3 days) and Midwest (+2 days).

Thirty-eight of the 50 largest metros saw time on market increase compared to the previous year. Time on market declined most in New Orleans (-21 days) as last year’s figure was impacted by Hurricane Ida. The other markets where time on market declined included Richmond (-15 days), Birmingham (-6 days), and Milwaukee (-5 days). Time on market increased most in the southern and western metros of Raleigh (+27 days), Austin (+26 days), Las Vegas (+21 days) and Phoenix (+21 days).

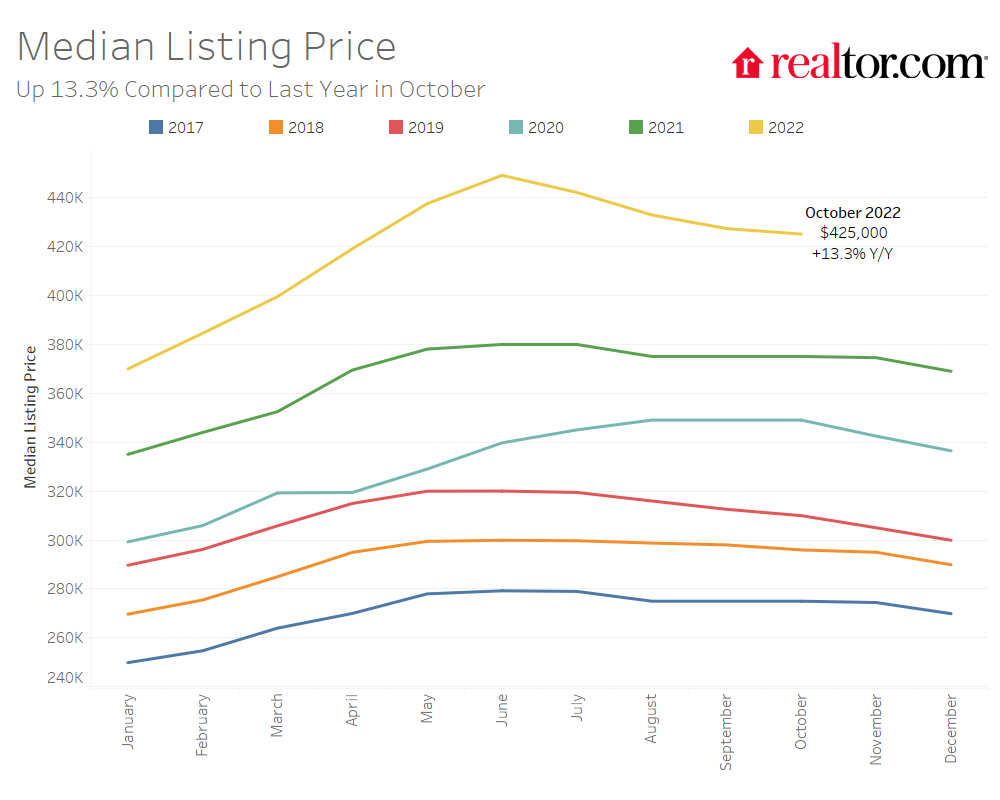

Price Growth Continues to Slow but Remains in Double-Digits

The median national list price declined to $425,000 in October, down from an all-time high of $449,000 in June. This represents an annual growth rate of 13.3%, a slight deceleration from last month’s growth rate of 13.9% and down from a peak growth rate of 18.2% in June.

The share of homes having their price reduced grew from 10.6% last October to 20.9% this year. The share is now well above 2017 (18.1%) and 2019 (17.0%) levels but is just below the share of price reductions in October 2018 (21.2%).

Active listing prices in the nation’s largest metros grew by an average of 9.2% compared to last year. Midwestern metros led the charge in active listing price growth, growing by 12.9% on average over the past year. Listing prices in the midwestern and southern metros of Milwaukee (+34.5%), Miami (+25.1%) and Kansas City (+21.4%) grew the most among large metros. Western metros saw the greatest increase in the share of price reductions (+18.9 percentage points), followed by southern metros (+13.6 percentage points). Homes in Phoenix (+35.9 percentage points), Austin (+31.2 percentage points), and Las Vegas (+24.4 percentage points) showed the greatest growth in the share of homes with price reductions compared to last year.

October 2022 Regional Statistics (50 Largest Metro Combined Average)

October 2022 Housing Overview by Top 50 Largest Metros

Note: With the release of its September 2022 housing trends report, Realtor.com® incorporated a new and improved methodology for capturing and reporting housing inventory trends and metrics. The new methodology updates and improves the calculation of time on market and improves handling of duplicate listings. Most areas across the country will see minor changes with a smaller handful of areas seeing larger updates. As a result of these changes, the data released since October 2022 will not be directly comparable with previous data releases (files downloaded before October 2022) and Realtor.com® economics blog posts. However, future data releases, including historical data, will consistently apply the new methodology.

Subscribe to our mailing list to receive updates and notifications on the latest data and research.

Join our mailing list to receive the latest data and research.

October 2022 Housing Market Trends Report – Realtor.com News

(Visited 1 times, 1 visits today)