According to Realtor.com®’s March housing data, the inventory of homes for sale continued to grow higher than last year but this pace of growth declined slightly and inventory remained constrained compared to pre-pandemic levels. Sellers were listing in lower numbers than previous years but those who listed their homes gradually adjusted to softer market conditions, as growth in the median list price continued to slow. Despite slowing listing price growth and increased price reductions, high interest rates continued to create an affordability challenge for buyers as fewer homes went under contract compared to the previous year.

Inventory Growth Slowed as Increasingly Fewer Sellers Listed Compared to Last Year

There were 59.9% more homes for sale in March compared to the same time in 2022. This means that there were 211,000 more homes available to buy this past month compared to one year ago. The growth rate in inventory began to slow slightly, as fewer potential sellers opted to list their home for sale. This means that there were still fewer homes available to buy on a typical day in March than there were a few years ago.

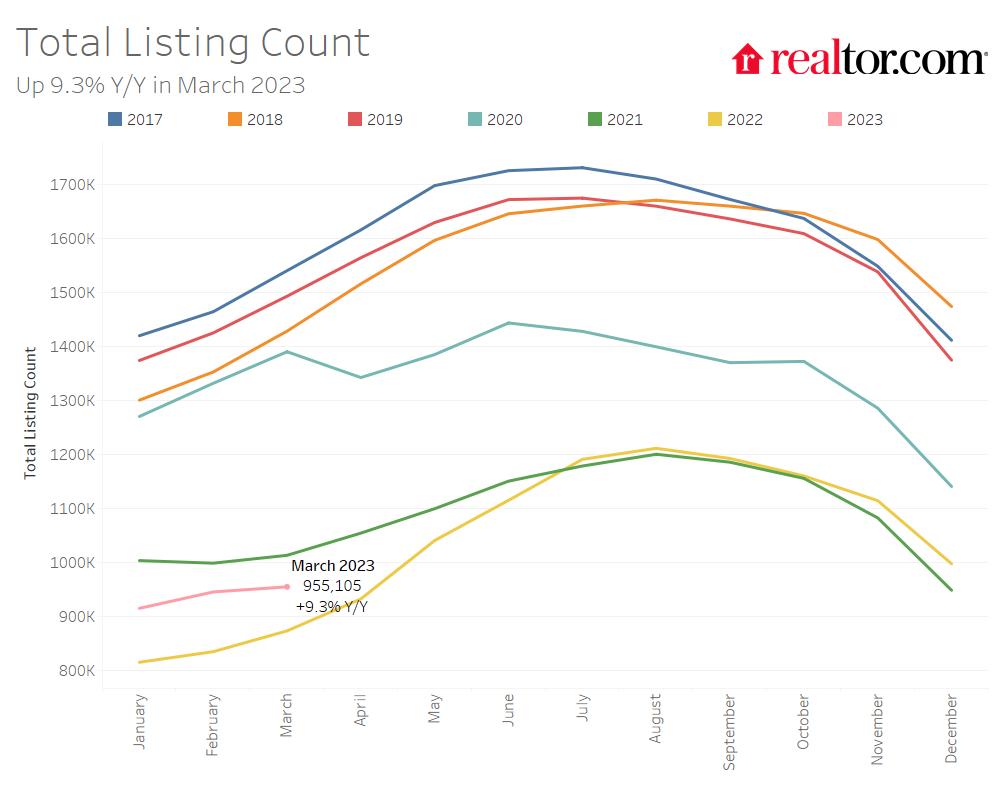

The total number of homes for sale, including homes that were under contract but not yet sold, increased by 9.3% compared to last year. Growth decelerated from last month’s 13.3% growth rate as fewer potential sellers listed homes. The growth rate in the total number of homes for sale also remains lower than active inventory because there were still fewer homes under contract (pending listings) than there were last year.

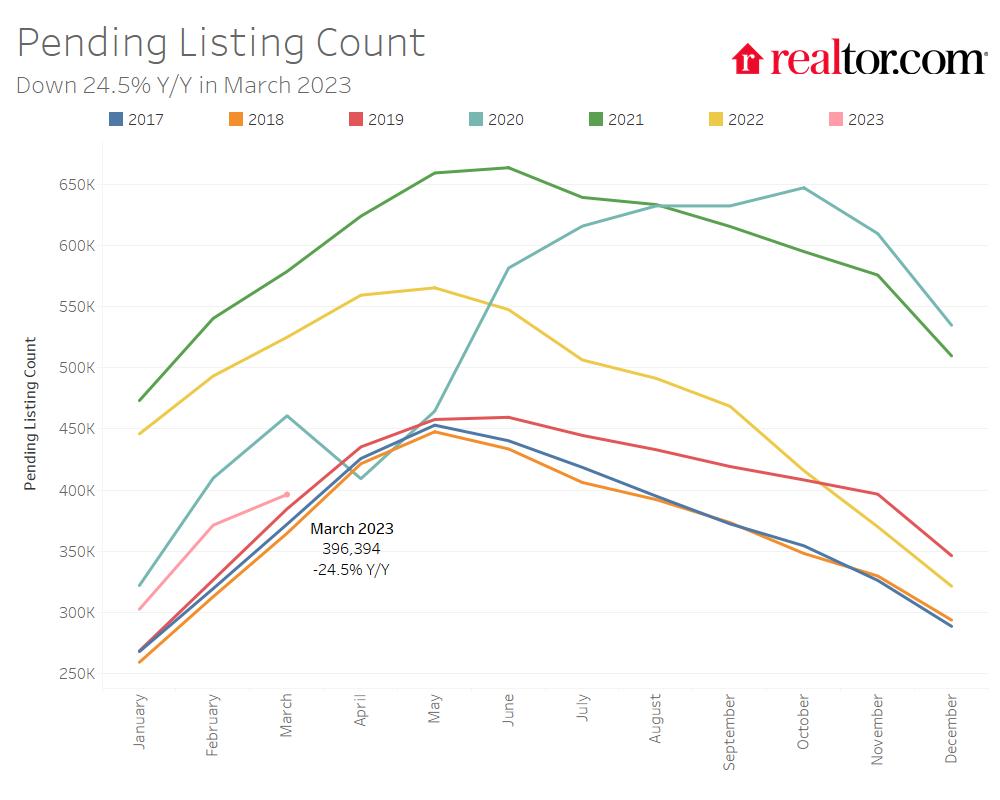

The number of homes under contract (pending listings) declined by 24.5% compared to the same time last year. This is similar to February’s 24.7% decline, which could mean that the housing market is starting to stabilize at a relatively low level of existing home sales activity. In the February Federal Open Market Committee meeting, the Federal Reserve Board decided to moderately increase its short-term policy rate by 25 basis points and noted that reduced credit accessibility could also help achieve the target inflation rate, signaling that their tightening campaign could be starting to wind down. Nevertheless, mortgage rates are expected to remain elevated in the near term. Higher rates and home prices compared to March of last year increased the monthly cost of financing 80% of the typical home by roughly $611 (+39.3%) compared to a year ago. This far outpaces recent rent growth (+3.1%) and inflation (+6.0%).

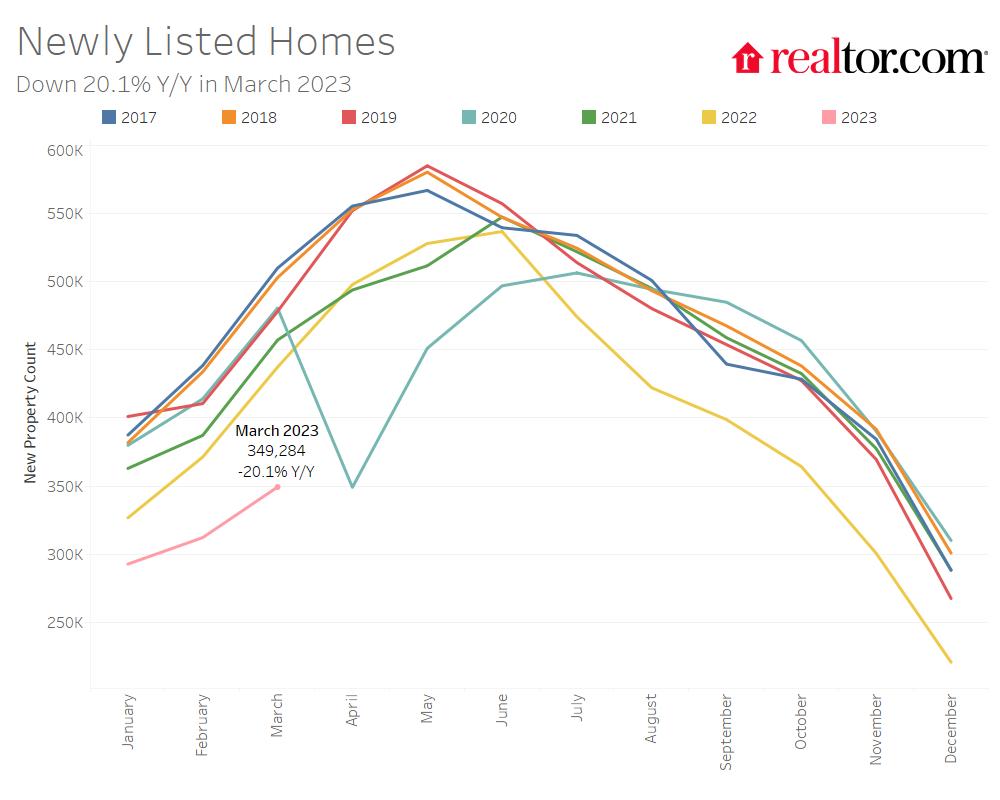

In March, the number of homes newly-listed for sale declined by 20.1% compared to the same time last year. This is a higher rate of decline than last month’s 15.9% decrease and new listings remained 29.7% below pre-pandemic 2017 to 2019 levels. In February, home selling sentiment declined due to declining price expectations, and it remained well below last year’s levels, according to Fannie Mae’s Home Purchase Sentiment Index (HPSI) survey. The net share of survey respondents who said now is a good time to sell decreased by 5 percentage points compared to the previous month and declined by 18 percentage points compared to the prior year.

The number of homes for sale in the 50 largest metro areas in the U.S. increased by 74.4% compared to last year. This was more than the national average. However, inventory in this group of metro areas as a whole is still 43.2% below pre-pandemic levels.

The Southern region saw the most growth in the number of homes for sale, with a 127.4% increase compared to last March. However, home inventory in the South was still 38.8% below pre-pandemic levels. The western region saw the second-most growth, with a 58.2% increase compared to last year. Inventory in the West was 32.3% below pre-pandemic levels. The Midwest and Northeast regions saw slower growth, with 24.3% and 11.9% increases over last March, respectively. Inventory in the Midwest was still 52.8% below pre-pandemic levels, and it was 60.6% below pre-pandemic levels in the Northeast.

In March, no regions saw an increase in selling activity. The South saw selling activity decline least, with newly listed homes down by 9.1% compared to the previous year, while they declined by 32.6% in the West, 22.4% in the Midwest, and 27.2% in the Northeast. In all regions newly-listed homes remained well below the typical levels seen in 2017 to 2019.

Inventory increased in 47 out of 50 of the largest metros compared to last year. Metros which saw the most inventory growth include Austin (+312.2%), Raleigh (+273.7%), and Nashville (+253.3%). The only metros which saw inventory decline on a year-over-year basis were Milwaukee (-17.2%), Hartford (-17.0%), and New York (-0.9%). However, despite high inventory growth compared to last year, most metros still had a lower level of inventory when compared to pre-pandemic years. In fact, only Austin (+2.0%), and Las Vegas (+1.4%) saw higher levels of inventory in March compared to typical 2017 to 2019 levels.

In March, only 7 metros saw the number of newly listed homes increase compared to last year. Nashville (+7.4%), San Antonio (+6.4%) and Raleigh (+3.4%) had the largest year-over-year growth in newly listed homes. Markets which reported large yearly declines included Sacramento (-44.5%), Providence (-40.0%), and San Jose (-39.7%).

Homes Are Taking Longer to Sell, but Not as Long as Pre-pandemic Levels

The typical home spent 54 days on the market this March which is 18 days longer than the same time last year. Slower inventory turnover was primarily fueling the growth in actively listed homes but homes still spent 15 fewer days on the market this March than they did in the average March from 2017 to 2019.

In the 50 largest metropolitan areas in the United States, the typical home spent 46 days on the market, 16 days more than the previous March. This trend was seen across all regions, with larger metros in the South seeing the greatest increase (+20 days), followed by the West (+19 days), Midwest (+13 days) and Northeast (+10 days). Homes in Western metros were also spending 6 more days on the market than pre-pandemic times, but in all other regions homes were still selling more quickly.

All of the 50 largest metros saw an increase in time on market compared to the previous year. Time on market increased the most in Raleigh (+42 days), Kansas City (+37 days), and Austin (+37 days). Fourteen predominantly western markets saw homes spend more time on the market than typical 2017 to 2019 timing. Kansas City (+20 days), Las Vegas (+11 days), Los Angeles and San Francisco (+10 days each), saw the greatest increase in time on market compared to average 2017 to 2019 pacing.

Listing Price Growth Continued to Decline in March

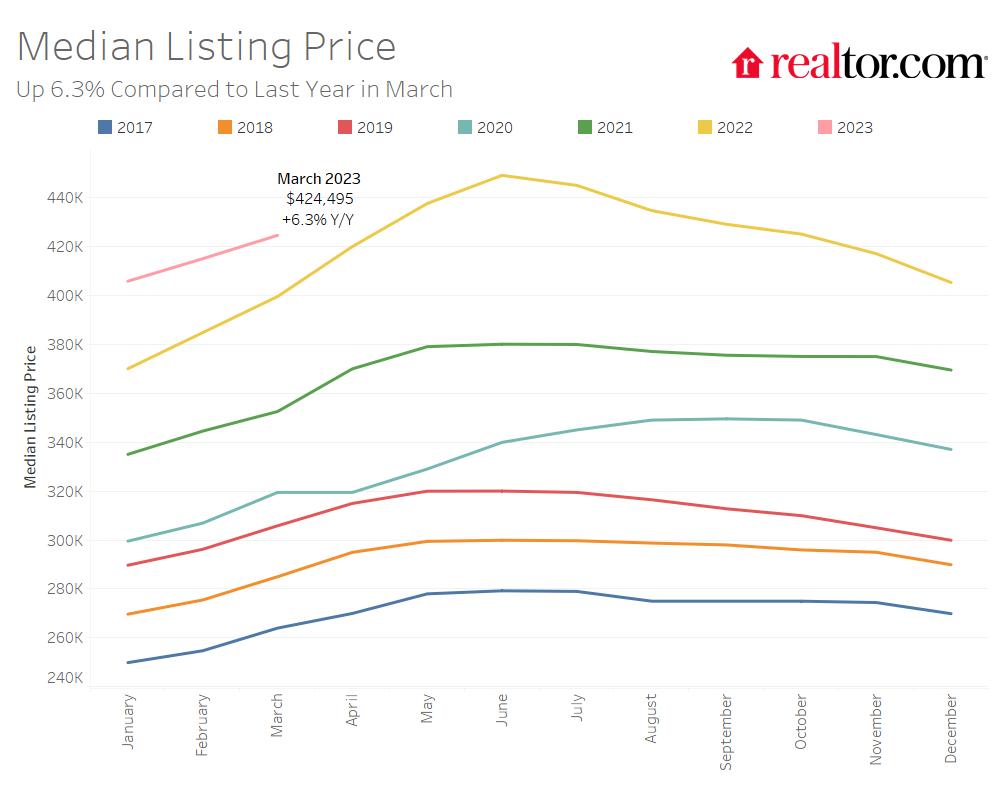

The national median list price grew to $424,000 in March, up from $415,000 in February. However, it was still down from a record high of $449,000 in June (-5.6%). This median list price represented a yearly growth rate of 6.3%, which is lower than February’s 7.8% growth rate and the lowest rate of growth since June 2020, in the early months of the COVID-19 pandemic. At this rate of slowing, list prices are likely to decline relative to the previous year by summertime, but the national median sale price already declined on an annual basis for the first time in over 10 years in February (by 0.2%).

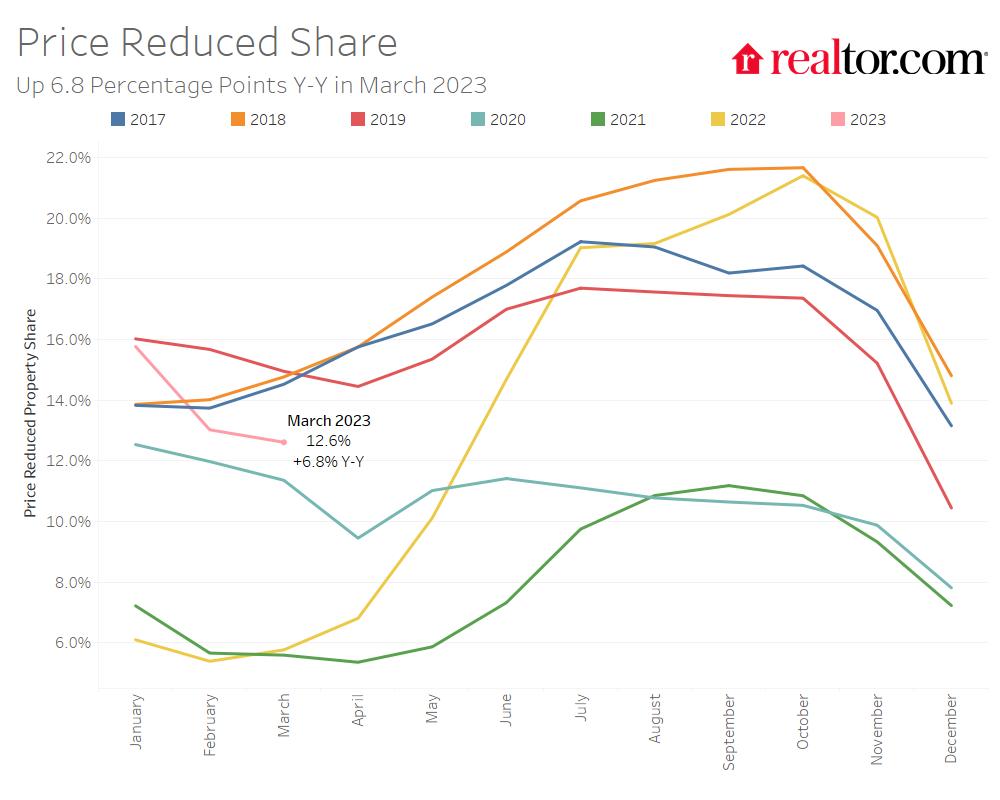

The percentage of homes with price reductions increased from 5.8% in March of last year to 12.6% this year. This share of price reductions, while much higher than last year, dipped below 2017 to 2019 pre-pandemic levels after reaching this threshold in January and continued to be lower in March, suggesting that while there is a bigger pricing gap between buyers and sellers relative to last year, sellers may be setting their initial asking price more in line with buyer expectations than was common before the pandemic.

In the largest metropolitan areas in the country, the combined annual median list price growth rate for active listings was 7.3%, slightly outpacing the national rate. Midwest metros had the highest growth rate in active listing prices, with an average increase of 11.2% over the past year. Prices in Memphis (+40.3%), Milwaukee (+26.3%), and Kansas City (+17.7%) saw the biggest increases among large metros. However, in each of these metros the mix of inventory changed as larger and more expensive homes were listed for sale in March compared to the previous year. On a price-per-square-foot basis, listing prices only grew by 17.4% in Memphis, 10.8% in Milwaukee, and 11.1% in Kansas City. Nine out of the largest 50 markets saw their median list price decline. The greatest price declines were seen in Austin (-8.4% year-over-year), Las Vegas (-6.7%), and New Orleans (-5.1%).

Large southern metros saw the largest increase in the percentage of homes with price reductions (+9.1 percentage points), followed by large western metros (+7.2 percentage points). Austin (+21.6 percentage points), Phoenix (+18.2 percentage points) and Tampa (+13.8 percentage points) had the largest increases in the percentage of homes with price reductions compared to last year.

March 2023 Regional Statistics (50 Largest Metro Combined Average)

March 2023 Regional Statistics vs Pre-Pandemic 2017-2019 (50 Largest Metro Combined Average)

March 2023 Housing Overview by Top 50 Largest Metros

*Some St. Louis listing metrics have been excluded while data is under review.

Subscribe to our mailing list to receive updates and notifications on the latest data and research.

Join our mailing list to receive the latest data and research.

March 2023 Housing Market Trends Report – Realtor.com News

(Visited 1 times, 1 visits today)