According to Realtor.com®’s February housing data, the inventory of homes for sale continued to grow, driven by homes spending more time on the market as buyers continued to face affordability constraints. A few larger metros also saw inventory increase above pre-pandemic levels. Selling activity continued to decline, with fewer newly listed homes compared to last year, despite an uptick in seller sentiment seen in January. Time on market continued to grow compared to last year but remained lower than pre-pandemic levels in all regions except for western markets. Price growth remains positive but continues to decline as sellers adjust expectations. There are some signals that price growth could be stabilizing as the market saw fewer price reductions as a share of total home inventory.

Las Vegas and Austin See Higher Inventory Compared to Pre-Pandemic Years

There were 67.8% more homes for sale in February compared to the same time in 2022. This means that there were 234,000 more homes available to buy this past month compared to one year ago. While the number of homes for sale is increasing, it is still 47.4% lower than it was before the pandemic in 2017 to 2019, nationwide. This means that there are still fewer homes available to buy on a typical day than there were a few years ago.

The total number of homes for sale, including homes that are under contract but not yet sold, increased by 13.3% compared to last year. Growth accelerated from last month’s 12.3% growth rate because homes are spending more time on the market, but the growth rate in the total number of homes for sale remains lower than active inventory because there are still fewer homes under contract (pending listings) than there were last year.

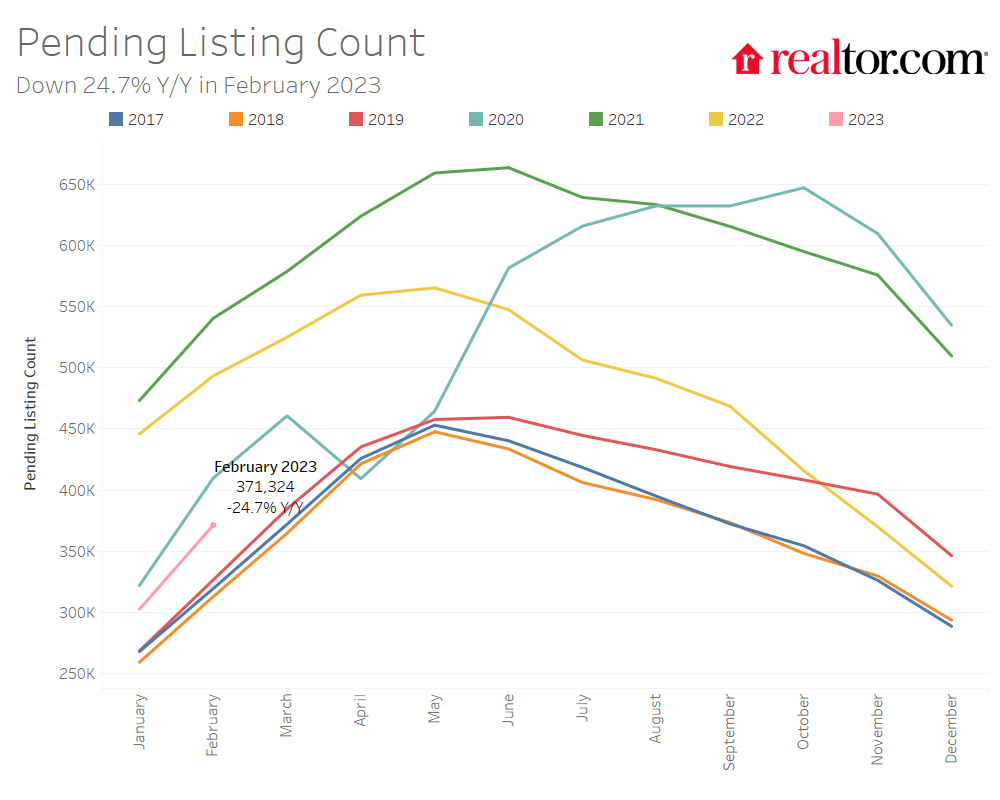

The number of homes under contract (pending listings) declined by 24.7% compared to the same time last year. This is smaller than January’s 32.1% decline, which could mean that the housing market is starting to stabilize at a relatively low level of existing home sales activity. In fact, other data on pending home sales point to a similar potential stabilization. However, this could change if the direction of inflation and mortgage rates changes in the months to come. While mortgage rates are down from October and November 2022, higher rates and home prices compared to February of last year have increased the monthly cost of financing 80% of the typical home by roughly $630 (+45.1%) compared to a year ago. This far outpaces recent rent growth (+2.9%) and inflation (+6.4%).

In February, the number of homes newly-listed for sale declined by 15.9% compared to the same time last year. This is a higher rate of decline than last month’s 10.4% decrease but it’s still an improvement from the declines seen in November and December. However, new listings remain 27.0% below pre-pandemic 2017 to 2019 levels. In January, home selling sentiment improved due to improved price expectations, however it remained well below last year’s levels, according to Fannie Mae’s Home Purchase Sentiment Index (HPSI) survey. The net share of survey respondents saying now is a good time to sell increased by 11 percentage points compared to the previous month but declined by 27 percentage points compared to the prior year.

The number of homes for sale in the 50 largest metro areas in the U.S. has increased by 86.0% compared to last year. This is more than the national average. However, inventory in this group of metro areas as a whole is still 40.9% below pre-pandemic levels.

The Southern region has seen the most growth in the number of homes for sale, with a 141.4% increase compared to last February. However, home inventory in the South is still 35.5% below pre-pandemic levels. The West region has seen the second-most growth, with an 82.9% increase compared to last year. Inventory in the West is only 26.8% below pre-pandemic levels. The Midwest and Northeast regions have seen slower growth, with 36.0% and 20.3% increases over last February, respectively. Inventory in the Midwest is still 51.5% below pre-pandemic levels, and it is 59.0% below pre-pandemic levels in the Northeast.

In February, no regions saw an increase in selling activity. The South saw selling activity decline least, with newly listed homes down by 7.0% compared to the previous year, while they declined by 31.4% in the West, 17.7% in the Midwest, and 17.0% in the Northeast. In all regions newly-listed homes remained well below the typical levels seen in 2017 to 2019.

Inventory increased in 49 out of 50 of the largest metros compared to last year. Metros which saw the most inventory growth include Austin (+335.1%), Raleigh (+329.8%), and Nashville (+299.7%). The only metro to see inventory decline on a year-over-year basis was Hartford (-8.8%). However, despite high inventory growth compared to last year, most metros still have a lower level of inventory when compared to pre-pandemic years. In fact, only Las Vegas (+9.4%), Austin (+2.6%) and San Antonio (+0.6%) saw higher levels of inventory in February compared to typical 2017 to 2019 levels.

In February, only 6 metros saw the number of newly listed homes increase compared to last year. Raleigh (+14.8%), Dallas (+10.3%) and San Antonio (+10.2%) had the largest year-over-year growth in newly listed homes. Markets which reported large yearly declines in newly listed homes were led by western metros such as San Jose (-43.3%), San Francisco (-39.4%), and Seattle (-36.8%).

Los Angeles and Las Vegas See Slowest Pace of Home Sales Compared to Pre-Pandemic Period

The typical home spent 67 days on the market this February which is 23 days longer than the same time last year. Slower inventory turnover is primarily fueling the growth in actively listed homes but homes still spent 20 fewer days on the market this February than they did in the average February from 2017 to 2019.

In the 50 largest metropolitan areas in the United States, the typical home spent 56 days on the market, 19 days more than the previous February. This trend was seen across all regions, with larger metros in the West seeing the greatest increase (+26 days), followed by the South (+23 days), Midwest (+15 days) and Northeast (+8 days). Homes in Western metros are also spending 10 more days on the market than pre-pandemic times, but in all other regions homes are still selling more quickly.

Out of the 50 largest metros, 47 saw an increase in time on market compared to the previous year. Time on market increased the most in Austin (+52 days), Raleigh (+51 days), Denver and Las Vegas (+42 days each). Only Hartford saw time on market decline, by 2 days. Meanwhile, Cincinnati and Buffalo saw no change compared to last year. Fifteen predominantly western markets saw homes spend more time on the market than typical 2017 to 2019 timing. Las Vegas (+17 days), Los Angeles (+15 days), Phoenix and Seattle (+11 days each) saw the greatest increase in time on market compared to average 2017 to 2019 pacing.

Listing Price Growth Continued Decline in February

The national median list price grew to $415,000 in February, up from $406,000 in January. However, it is down from a record high of $449,000 in June (-7.6%). This median list price represents a yearly growth rate of 7.8%, which is lower than January’s 9.7% growth rate. While the growth rates in December and January appeared to have stabilized at 9.7%, February marks a continuation of declining price growth.

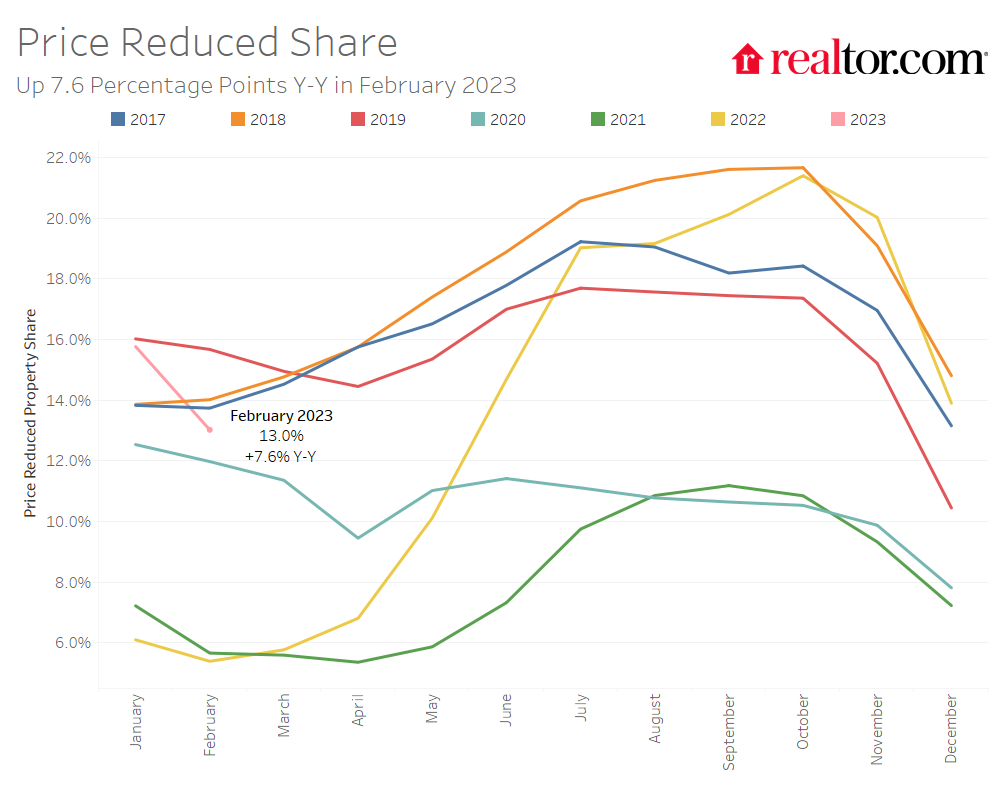

The percentage of homes with price reductions increased from 5.4% in February of last year to 13.0% this year. This share of price reductions, while much higher than last year, dipped below 2017 to 2019 pre-pandemic levels after reaching this threshold in January. Moreover, the drop in the share of price reductions from January to February appears to be larger than typical seasonal movements. In the past we have seen price reductions act as a leading indicator to median list price growth. While only one month does not make a trend, this could signal a cushion for price growth.

In the largest metropolitan areas in the country, the combined annual median list price growth rate for active listings was 6.4%. Midwest metros had the highest growth rate in active listing prices, with an average increase of 11.9% over the past year. Prices in Milwaukee (+48.8%), Memphis (+42.7%), and Virginia Beach (+16.3%) saw the biggest increases among large metros. However, in each of these metros the mix of inventory has changed and more larger, expensive homes are for-sale today. On a price-per-square-foot basis, listing prices only grew by 22.6% in Milwaukee, 18.4% in Memphis, and 7.8% in Virginia Beach. Eight out of the largest 50 markets are seeing the median list price decline. The greatest price declines were seen in Austin (-8.0% year-over-year), New Orleans (-7.0%), and Pittsburgh (-6.9%). In each of these markets, the median price-per-square-foot also declined on a yearly basis, signaling that price declines in these markets were not caused by an increase in smaller listings but by sellers beginning to adjust expectations to softer housing market conditions.

Large southern metros saw the largest increase in the percentage of homes with price reductions (+10.3 percentage points), followed by large western metros (+8.6 percentage points). Austin (+21.2 percentage points), Phoenix (+19.2 percentage points) and Las Vegas (+15.1 percentage points) had the largest increases in the percentage of homes with price reductions compared to last year.

February 2023 Regional Statistics (50 Largest Metro Combined Average)

February 2023 Regional Statistics vs Pre-Pandemic 2017-2019 (50 Largest Metro Combined Average)

February 2023 Housing Overview by Top 50 Largest Metros

Note: With the release of its February 2023 Housing Report, Realtor.com® incorporated a new and improved methodology for capturing and reporting housing inventory trends and metrics. As a result of these changes, this release is not directly comparable with previous data releases and reports. However, future data releases, including historical data, will consistently apply the new methodology.

Subscribe to our mailing list to receive updates and notifications on the latest data and research.

Join our mailing list to receive the latest data and research.

February 2023 Housing Market Trends Report – Realtor.com News

(Visited 1 times, 1 visits today)