With a market cap of nearly $3 trillion, Apple (NASDAQ:AAPL) remains the world’s most valuable company, thanks to its unmatched combination of products and services that make up the tech giant’s ever-expanding ecosystem.

However, it has not all been easy going recently. In Apple’s recently reported fiscal fourth quarter results, total revenue dropped by 1% year-over-year to $89.5 million. That said, even against a backdrop of falling revenue, iPhone sales and Services revenue reached record levels, and its active installed base of devices across all products and geographies attained new all-time highs.

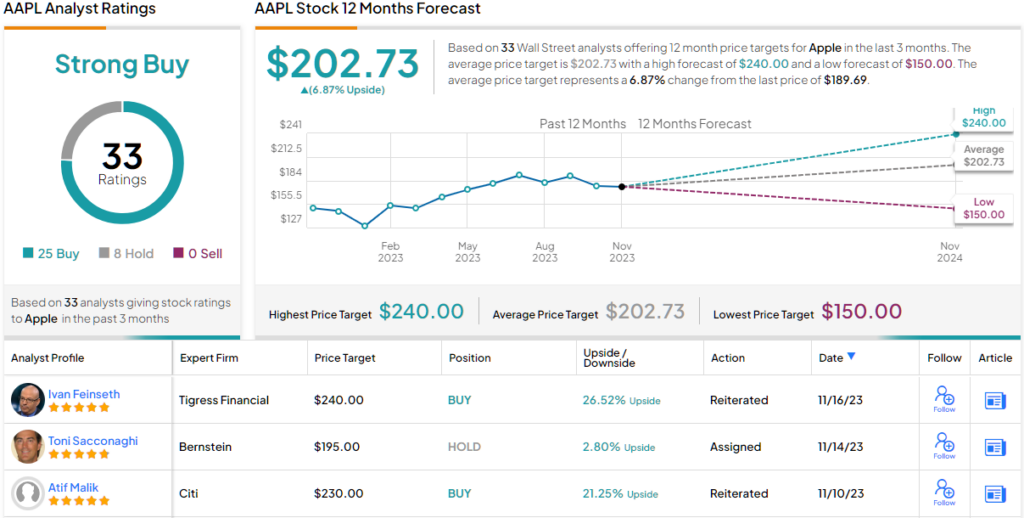

These are points made by Tigress Financial’s Ivan Feinseth, a 5-star analyst rated in the top 5% of the Street’s stock pros, who believes AAPL’s “industry-leading position and strong brand equity, driven by its innovative ability and powerful cash generation, will continue to generate an increasing Return on Capital, driving the ongoing growth of Economic Profit and shareholder value creation.”

In fact, with such sound prospects ahead, Feinseth has now raised his price target for Apple shares from the prior $225 to a Street-high of $240, suggesting the stock will gain 26.5% over the coming months. Feinseth’s rating stays a Strong Buy. (To watch Feinseth’s track record, click here)

As noted above, despite the strong iPhone sales and Services revenue in the quarter, overall revenue fell slightly, and that is a result mainly of decelerating hardware sales. The good news, according to Feinseth, is that is all about to change.

The company recently introduced its new iMac and MacBook Pro, showcasing the cutting-edge M3 third-generation processor, which was developed in-house. Emphasizing top-notch performance and capabilities, the new processor series takes advantage of Apple’s advanced 3nm manufacturing technology to drive “incredibly fast” graphics processing.

That represents some good timing on Apple’s part, as the launch coincides with an anticipated recovery next year in demand for PCs, the expected sales growth coming off the back of “several years of declines.”

Growth is expected to come from elsewhere too. The soon-to-be released Apple Vision Pro (expected to launch in the first quarter of next year) is a spatial computer offering a combination of digital content and the physical world. Consisting of unique features that allow it to perform as a computer, TV screen, and gaming platform, Feinseth expects it “will evolve into a major product category.”

Feinseth is evidently a fully-fledged AAPL bull, but how does the rest of the Street see the next year panning out for Apple stock? Most are bulls too. Based on a mix of 25 Buys vs. 8 Holds, the stock claims a Strong Buy consensus rating. That said, following this year’s gains of 52.5%, the upside appears capped; the $202.73 average target represents modest returns of ~7% from current levels. (See Apple stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.